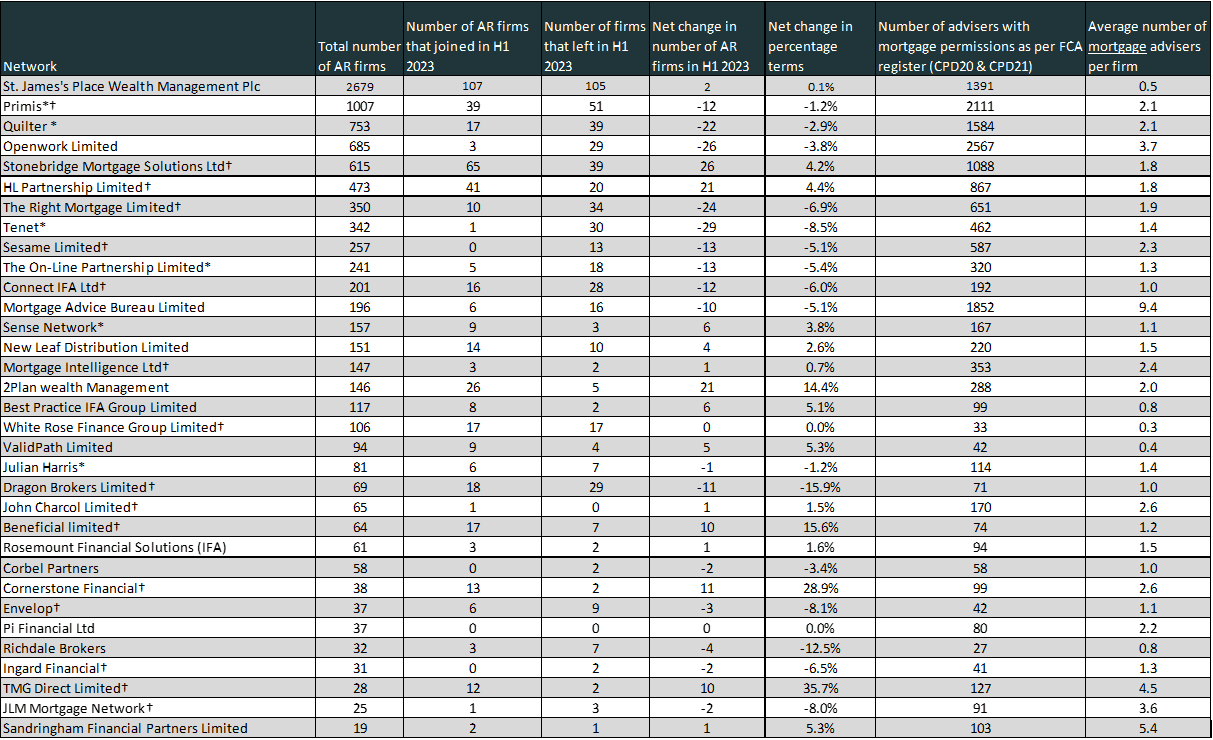

Network League Table - H1 2023

For more information on networks click Network Directory below

The data source for the table below is the FCA register and was correct at 5th July 2023.

It illustrates the movement of Appointed Representative firms for each network over the period 1st January 2023 to 30th June 2023.

It is prioritised by total number of AR Firms, adviser numbers for this table only include mortgage advisers.

The size of a network does not mean they will be best for you. If you're looking for a network, please get in touch and let us help find the best one for YOU.

* Denotes networks with multiple networks under one brand.

† Denotes dedicated mortgage networks.

CPD20 mortgage advisers, CPD21 equity release.

For more detail regarding the table, please go to the Network League Table overview

As always, this table should not be used as an indication of which networks are “best” it is purely to illustrate the movement of Appointed Representative Firms (AR’s) firms in a given time period and highlight network trends.

In terms of AR movement, Q1 saw a differential of nearly 100 more firms leaving the main networks than joining. There was some speculation at the time that this could be down to the implantation of the AR Regime and perhaps additionally, a result of preparation work for Consumer Duty. However, the figures for the first half of 2023 show that the Q2 was much more positive, as the data now shows a reduction in the number of firms leaving. This figure has now reduced to 60 more firms leaving the main networks than joining, this illustrates that Q2 had a positive figure of 39 more firms joining than leaving. It will be interesting to see how this pans out over the year.

In terms of net gains, the strong performers in 2023 year-to-date are Stonebridge with a net gain of 26 new AR firms, 2Plan with 21 new firms and HL Partnership also with 21 new AR firms. The latter was bolstered by its recent purchase of smaller network AFP partnership, taking its AR’s in to the HLP fold. There is also notable growth in percentage terms with two networks being well ahead of the rest of the field, that being TMG Network and Cornerstone with a net growth of 35.7% and 28.9% respectively.

As noted in the key below the table, there are many networks that have multiple propositions under one main brand. Every one of these brands each have their own AR firms and are collectively shown in the table under the main brand. In previous tables we’ve counted every firm under each brand, although some networks had firms that are dual authorised under two of their brands. To give a greater level of accuracy, any dual authorised firms are now only counted once in the total number. In actual fact this only affects two networks that appear in the table, the more notable being Quilter who have seen a three figure reduction in previously reported numbers.

Dual authorisation can come in to play if a firm has both wealth and mortgage advisers, wish to separate the two areas of advice and are with a network that will allow them to be dual authorised. Networks that have offerings for both wealth and mortgage & protection are in a position to offer dual authorisation under the auspices of one group.

There is still plenty movement of advisers and firms looking for a home or changing principal, although those specialising in mortgages have been distracted from their plans to move due to the level of work caused by interest rate changes and product removals. From our own conversations there are an encouraging number of advisers either entering or re-entering the marketplace. I am really interested to see what the movements look like for the remainder of 2023 and beyond.