2025 AR Firm Dynamics: Growth, Decline, and Shifting Market Structures

The latest data compiled by Network Consulting paints a nuanced picture of the UK’s appointed representative (AR) landscape as of January 2026. While headline figures show a modest overall increase of 89 AR firms across networks in 2025, the underlying trends reveal a more complex and evolving market.

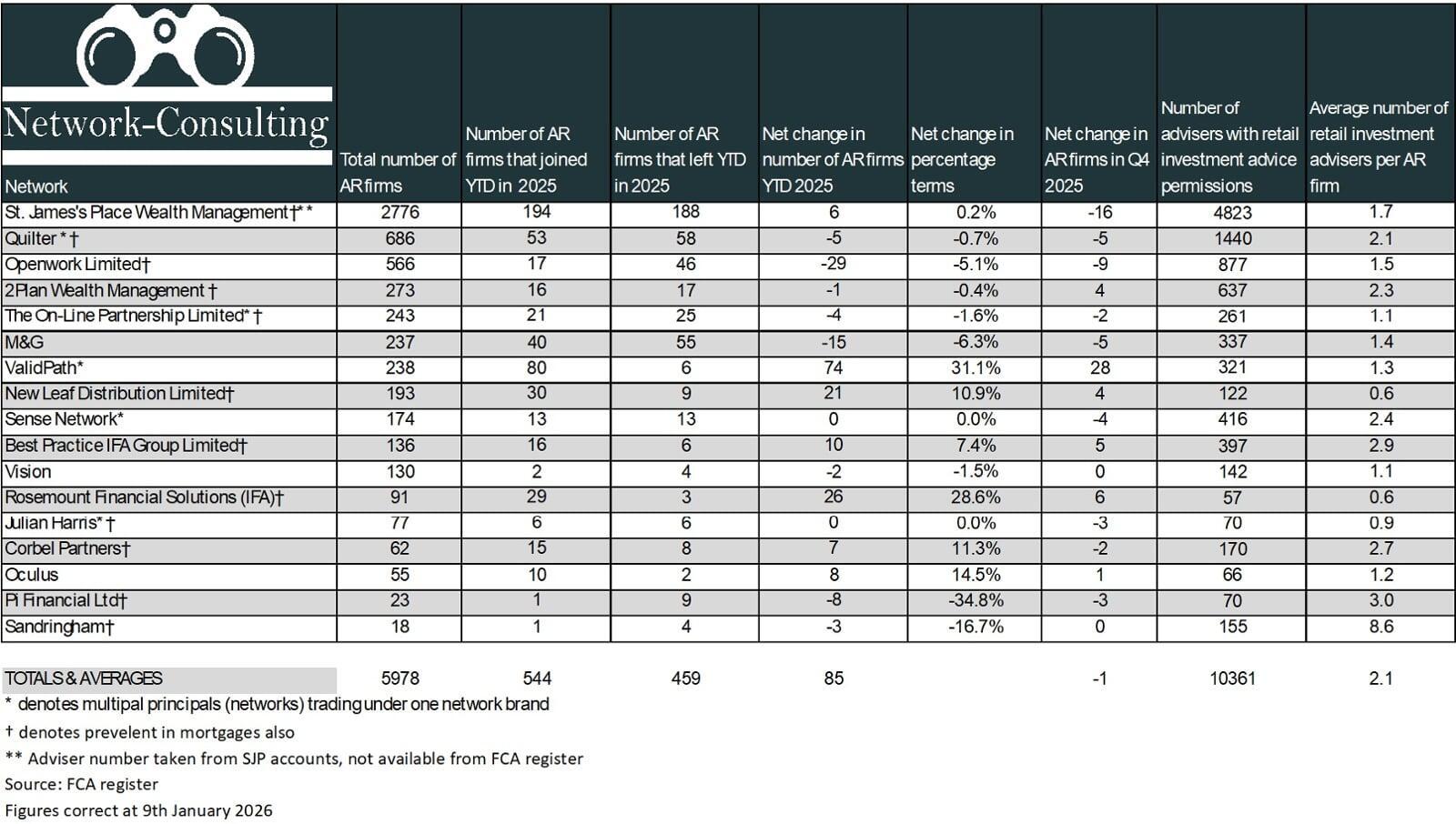

St. James’s Place Wealth Management (SJP) continues to dominate in terms of scale, boasting 2,776 AR firms, by far the largest network footprint. It also recorded the highest number of new AR firms joining in 2025 (194), although its net growth was minimal at just six firms. This gain is largely attributed to its academy programme, which consistently feeds new entrants into the network.

In contrast, ValidPath Limited emerged as the standout performer in net growth terms, adding 80 firms, an impressive 31.1% increase, although figures for 2025, now include a separate brand of Valid Path Financial Limited, both under the tradign label of Valid Path. Rosemount Financial Solutions and New Leaf Distribution also posted strong gains, with growth rates of 28.6% and 10.9% respectively. Notably, both networks are active in mortgage protection, suggesting that dual-sector engagement may be a contributory factor in their expansion.

On the other end of the spectrum, Openwork Limited experienced the steepest decline, shedding 29 (Net) AR firms over the year. M&G and Pi Financial also saw significant contractions, with Pi Financial’s 34.8% drop representing the largest percentage loss among all networks, although this was only 8 firms form its modest number of AR firms.

Beyond individual network performance, broader structural shifts are underway. A recent Freedom of Information response from the FCA, obtained by Network Consulting, reveals a sharp contraction in the Directly Authorised (DA) retail advice space between 2020 and 2025. DA firms operating in both wealth and mortgage sectors declined by 24.4%, equating to a loss of 957 firms. Wealth-only DA firms fared little better, falling by 19.4%, a reduction of 1,054 firms.

These figures suggest a growing preference among advisers for network affiliation, potentially driven by regulatory pressures, Consumer Duty requirements, a more arduous application process and perhaps threshold requirements. While networks are gaining ground, the shrinking DA segment raises questions about long-term market diversity and adviser autonomy.

As the industry continues to adapt to regulatory change and shifting adviser preferences, the AR model appears to be consolidating its position as a dominant force in UK retail financial advice. Whether this trend continues will depend on how networks balance growth with quality, and how the FCA responds to the evolving landscape.