Network Consulting Services has released its Q1 2026 Wealth-Focused Network League Table, providing insight into adviser firm movement across the UK financial advice sector during a period of continued regulatory change, strategic restructuring and growing operational scrutiny.

The latest data highlights a market increasingly shaped by Consumer Duty requirements, ongoing focus on adviser servicing standards and growing demand for scalable compliance and technology infrastructure.

While several of the sector’s largest networks continue to operate at significant scale, the figures suggest adviser firms are increasingly reassessing long-term proposition suitability, operational flexibility and strategic alignment.

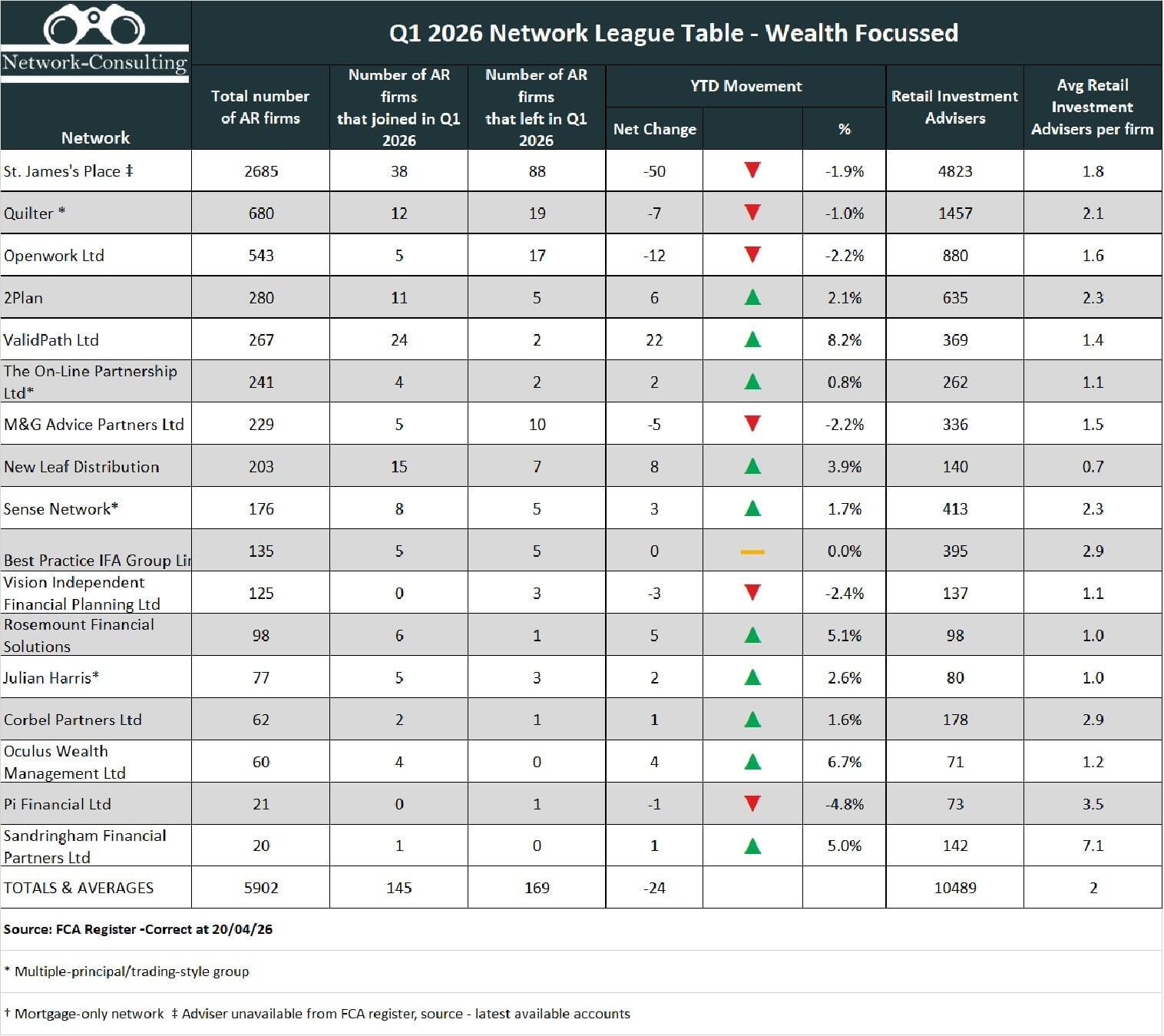

St. James’s Place, Quilter and Openwork all remain major participants within the market, although each recorded net reductions in appointed representative firms during the quarter. Industry observers note that this reflects a broader trend of firms reviewing their operating structures, servicing obligations and long-term commercial positioning in response to changing regulatory expectations.

At the same time, a number of mid-sized and expanding propositions reported positive growth during Q1 2026. ValidPath recorded one of the strongest net increases within the period, while New Leaf, Rosemount and 2Plan also saw positive adviser firm movement as firms continue to seek flexible operating models supported by robust compliance and operational support.

Best Practice IFA Group parent company, Schroders, agreed a sale to Nuveen, although it is uncertain as to what this spells out for the network at this stage. Julian Harris, appeared to leap up in AR numbers but this was explained by a name change of one brand from Julian Harris Mortgages to Julian Harris Adviser Network, with the simultaneous dual registration of firms within Julian Harris Financial Consultants. The true growth of new firms is reflected in the table below.

The evolving regulatory landscape continues to influence adviser and network strategy across the sector. Ongoing FCA focus on Consumer Duty, fair value assessments and evidencing customer outcomes has increased scrutiny around servicing standards, operational resilience and remuneration structures across wealth and protection propositions alike.

Industry observers also note growing discussion around pricing transparency and long-term customer value within protection and insurance distribution, as firms continue adapting to changing regulatory expectations and increasingly outcome-focused supervision.

Tthe latest figures reflect a market undergoing structural evolution rather than short-term movement alone. The wealth advice sector continues to evolve at pace. Consumer Duty, ongoing servicing expectations and increasing regulatory oversight are all influencing how firms assess network propositions and future business strategy.

What we are seeing is a more considered and strategic approach from adviser firms. Decisions are increasingly being driven by operational resilience, technology capability, succession planning, culture, contractual exit terms and long-term sustainability alongside purely commercial considerations.