UK Mortgage Network Movements – YTD and Q2 2025 Summary

As we pass the halfway point of 2025, the UK mortgage and protection network sector continues to evolve with measured confidence showing nuanced shifts in appointed representative (AR) firm activity. Year-to-date (YTD) figures point to a broadly stable landscape, with several networks achieving growth through focused recruitment, adviser expansion, and new firm onboarding, while others contend with net attrition.

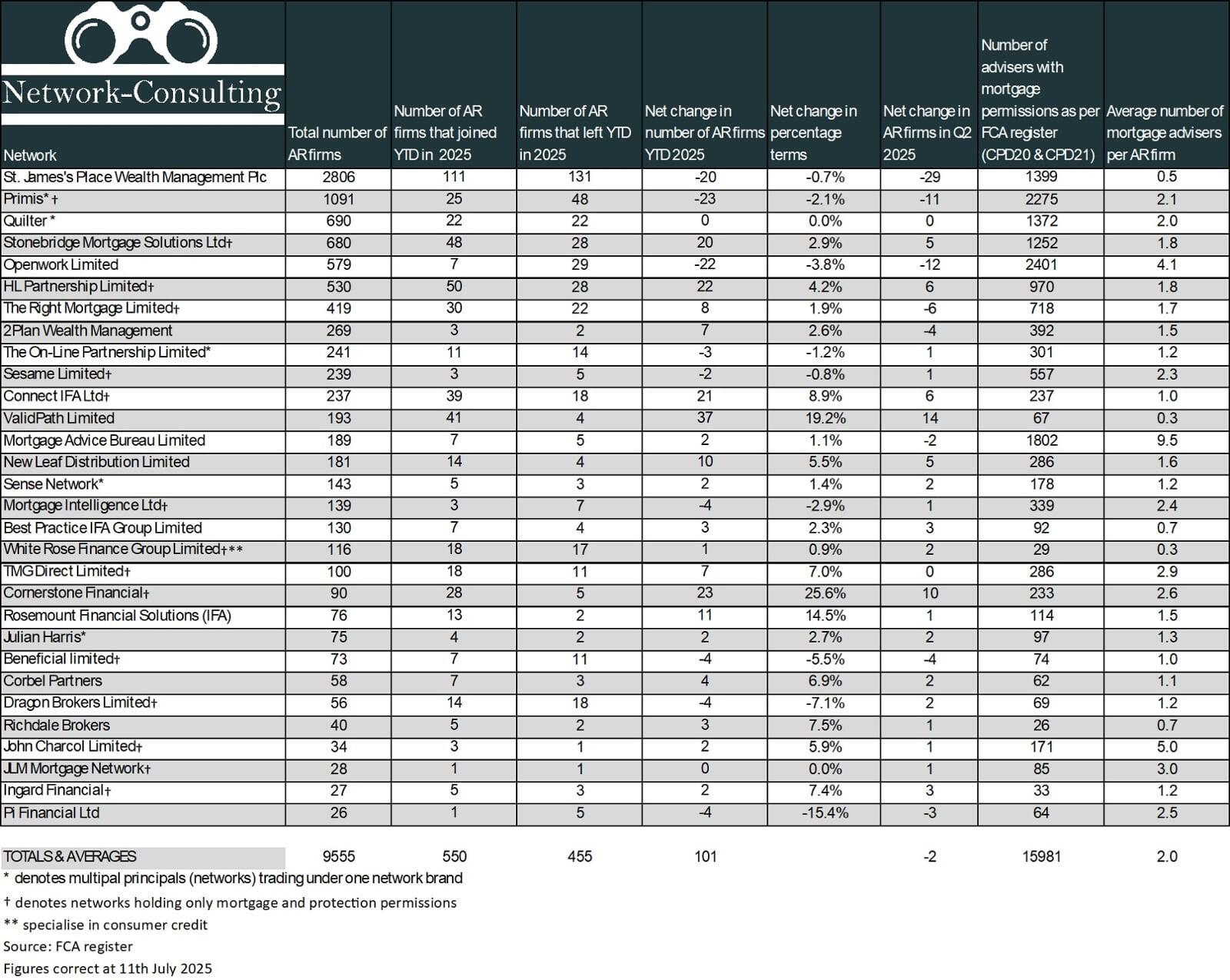

AR firm numbers across the top 30 networks have remained notably consistent, with only a marginal net shift of -1 compared to Q1. However, the mortgage adviser headcount within these networks experienced a net increase of 227 for the second quarter. This indicates healthy organic growth and a continued appetite for scaling within existing AR businesses. This shift points to an increasingly efficient use of the network model, where firms are deepening capacity rather than simply expanding footprint.

On initial assessment of the data, it appeared as though Quilter had enjoyed a massive gain of hundreds of AR firms. However, closer inspection revealed that these movements stemmed from internal realignment between group brands on the FCA register, resulting in no net change in firm numbers across the network.

Notable YTD growth by the standout performers amongst mortgage dedicated networks are firstly, Cornerstone Finance with the highest net increase of AR firms with 23, representing a 25.6% uplift. Similarly, Rosemount Financial Solutions had an impressive increase of 14.5% while HL Partnership, Connect and Stonebridge all enjoyed net increase of 22, 21 and 20 firms respectively.

On the contraction side, several well-established networks saw continued reductions, most notably Openwork, which delivered a net loss of 22 AR firms YTD and -12 in Q2, extending a downward trend that has persisted since Q1 2023. Primis also experiencing similar net decline, losing 23 firms YTD and 11 in Q2, although in isolation these numbers only represent small losses in percentage terms for the two networks.

Despite some notable shifts in AR numbers across the sector, significant investments and appointments underscore a vote of confidence in the network model. Openwork’s £120m strategic partnership with Bain Capital valuing a 30% stake highlights its commitment to scaling adviser support through technology and infrastructure, even amid contraction in AR numbers. HL Partnership’s multimillion-pound investment in Haysto further reflects drive to back digital innovation in the sector. Meanwhile, key leadership appointments, including Ben Allen as Managing Director of The Right Mortgage, formerly the Compliance Director and Dan Hobbs stepping into the CEO role at New Leaf Distribution signal a fresh strategic direction for the two long standing networks.

While Direct Authorisation remains a vital route for many firms, the network model continues to offer scalable compliance, strategic alignment, and commercial strength for those seeking resilience in a shifting regulatory environment. The FCA appears increasingly wary of a fragmented retail landscape dominated by numerous standalone DA firms. However, its focused attention and scrutiny of networks illustrates that they need them to be fit for purpose. Yet, it also reflects their commitment to the model and potential to deliver strong governance, fair adviser oversight, and better client outcomes. For well-run networks, that scrutiny translates into opportunity, where a culture of best practice turns regulatory rigour into long-term dividends with strong firm partnerships.