Network Growth Outpaces DA Market for Another Year, New Data Shows

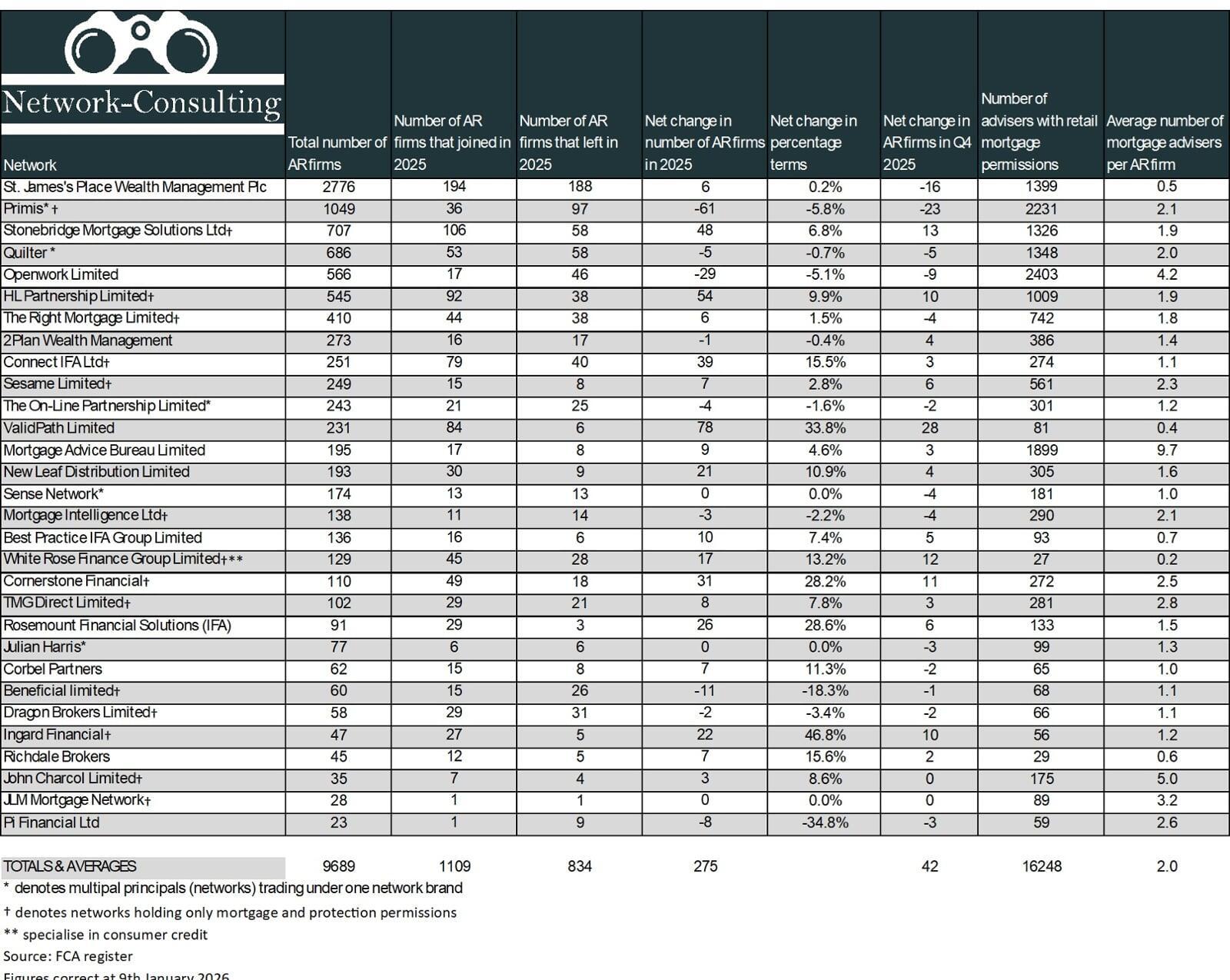

The mortgage network sector continued its upward trajectory in 2025, recording a net increase of 275 Appointed Representative (AR) firms across the top 30 networks holding mortgage permissions. This growth stands in stark contrast to the directly authorised (DA) market, which contracted by 247 firms and 516 advisers over the same period, according to figures released last week by Network Consulting from a recent response to a Freedom of Information request to the FCA (https://www.mortgagestrategy.co.uk/news/da-contraction-vs-network-growth-the-new-market-divide/).

The data received from the FOI clearly illustrates that this divergence is not a one-off anomaly. The DA space has been steadily constricting over recent years, while the AR sector remains resilient, stable, and consistently growth-positive. While going DA is clearly the right choice for some firms, the data reflects a broader shift in adviser preferences, regulatory appetite, and operational support structures, with many firms opting for the infrastructure and compliance backing that networks provide.

When we look at the table, among the standout performers in 2025, ValidPath led the field with a net gain of 78 firms, a 33.8% increase. Although primarily focused on wealth advice, its expansion is notable in the AR space. For networks with a core mortgage proposition, HL Partnership delivered the strongest growth, adding 54 firms. Stonebridge, Connect, Cornerstone, and Rosemount also posted robust increases, each contributing meaningfully to the networks overall expansion.

Ingard achieved a 46.8% growth rate, adding 22 firms from a relatively small base. Best Practice, White Rose (primarily consumer credit), and Rosemount also posted double-digit percentage growth, reflecting strong recruitment and retention strategies across smaller networks.

Conversely, Primis recorded the largest net reduction, losing 61 firms, a decline of 5.8%. Despite this, Primis remains one of the sector’s largest players, with more than 1,000 firms and 2,231 mortgage advisers still within its footprint. Other networks with net losses included Openwork, Julian Harris, PI Financial, and Dragon Brokers.

It is important to note that this data does not indicate which networks are “best.” The table illustrates movement in AR firm numbers, not quality, compliance strength, or adviser satisfaction. Growth or contraction may reflect strategic repositioning, adviser migration, or network-level decisions, and should be interpreted in context.

As the sector continues to evolve, these figures offer a snapshot of market change, but not a verdict. Advisers considering their next move should look beyond headline numbers and assess networks based on compliance culture, commercial terms, technology, and long-term strategic fit.